Another financial year has just finished! As a business owner, there are many obligations that you need to consider and action after June 30. Some of these will help to minimise your tax:

Key changes from 1 July 2017

-

- The temporary budget repair levy for high income earners is abolished. This reduces the highest marginal tax rate from 49% to 47%.

- The maximum concessional contribution has been reduced to $25,000, independent of your age at the start of the financial year.

- The maximum non-concessional contribution has been reduced to $100,000.

- The maximum amount of non-concessional contributions allowed under the bring forward provisions has reduced to $300,000.

Confirmation of changes from 1 July 2016

The following were expected to be implemented from 1 July 2016, and we can confirm that the following measures have passed parliament and are now law:

SBE Company Tax Rate reduced to 27.5%

Effective 1 July 2016, the company tax rate for SBE (Small Business Entities) reduces by 1% from 28.5% to 27.5%. To be considered an SBE, your group aggregated turnover must be less than $10 million. This key concession for 2017 applies again in 2018.

$20,000 Immediate Deduction for SBE’s

Business groups with aggregated turnover of less than $10 million are now eligible to claim an immediate deduction for depreciating assets costing less than $20,000.

Similarly, depreciating assets costing $20,000 or more will be allocated to the SBE’s general small business pool and will depreciate at a rate of 15% in the income year in which the assets are first used or installed ready for use. The assets will then be depreciated as part of that pool at 30% in subsequent income years.

If the balance of the general small business pool is less than $20,000 at the end of the income year, this balance is also written off.

Capital gains tax changes for foreign investors

You might not need to do a Stocktake

Small Business Entities (operational businesses with an aggregated turnover below $10 million) have access to a range of tax concessions. One of these concessions is the simplified trading stock rules. Under these rules, you can choose not to conduct a stocktake for tax purposes if there is a difference of less than $5,000 between the opening value of your trading stock and a reasonable estimate of the closing value of trading stock at the end of the income year. You will need to record how you determined the value of trading stock on hand.

If you would like to take advantage of the simplified trading stock rules, call us today to make sure you are eligible to use the simplified rules and to discuss how to use them properly.

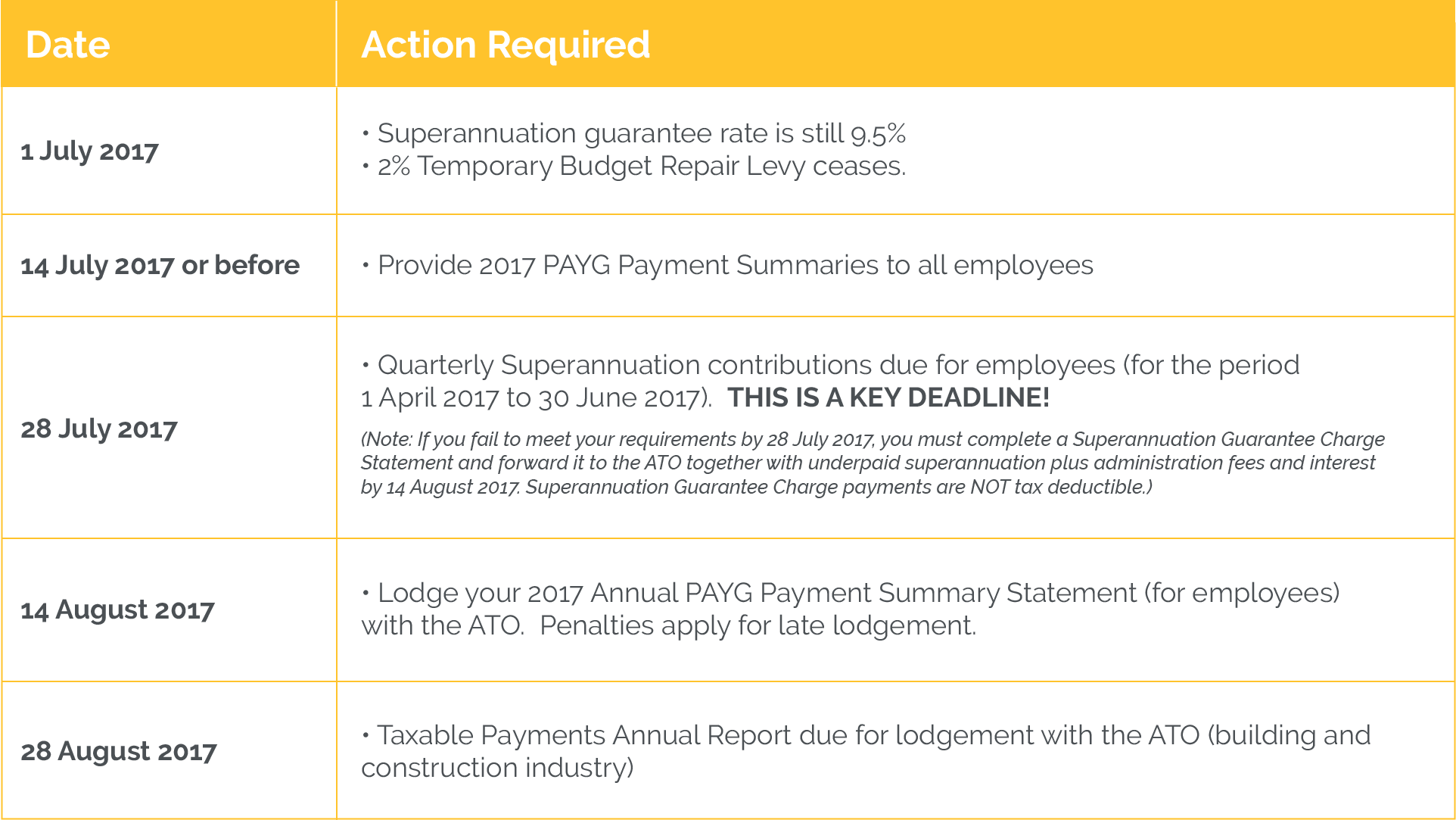

Deadline for 2017 PAYG Payment Summaries

You need to provide 2017 PAYG Payment Summaries to your employees and other workers by 14 July 2017. These must then be submitted to the ATO by 14 August 2017 or penalties will apply.

(Action Required) If you have any doubt about how to correctly complete your 2017 PAYG Payment Summaries, please contact us for assistance BEFORE you prepare them.

Building and Construction Industry Reporting

From 1 July 2012, new tax reporting rules apply for businesses in the building and construction industry. Businesses will have to lodge an annual report with the ATO setting out details of payments made to contractors. This will assist the ATO to reduce the “cash economy” by ensuring tax is paid on all income including “cash” payments.

You will need to record the following details of all payments made to contractors for building and construction services:

-

-

- The ABN of the contractor

- The name and address of the contractor

- The gross amount paid for the financial year, including GST

- The total GST included in the gross amount paid

-

If you use computerised accounting software, your system should be able to track this information for you and prepare the required Taxable Payments Annual Report.

(Action Required) Ensure that you lodge your Taxable Payments Annual Report with the ATO no later than 28 August 2017.

Payroll Tax

Payroll tax applies to all entities that have an Australian payroll that exceeds state-based limits. You should note that in addition to normal salaries and wages, the following items are generally also included in payroll expenses if payroll tax applies:

-

-

- fringe benefits based on the grossed-up taxable value of fringe benefits;

- all employer contributions to superannuation on behalf of employees; and

- some contractor or sub-contractor fees.

-

For more detailed information about whether payroll tax applies to your business, please contact our office.

(Action Required) The Annual Return/Reconciliation for payroll tax must be lodged by 21 July 2017 with your State Revenue Office.

WorkCover/WorkSafe

Your WorkCover/WorkSafe insurer sends an annual reconciliation to all registered employers at the end of the financial year.

In completing your annual reconciliation, you will need to include the following items in addition to normal salaries and wages:

-

-

- fringe benefits based on the taxable value of fringe benefits (do not gross-up);

- all employer contributions to superannuation on behalf of employees; and

- some contractor or sub-contractor fees.

-

For more detailed information about what items to include in the reconciliation statement, please contact our office.

Once the reconciliation is received and processed by your WorkCover/WorkSafe insurer, you will be issued with a final assessment or a refund depending on the instalments you have paid during the year.

(Action Required) Complete and lodge the Annual Reconciliation with your WorkCover/WorkSafe insurer by the due date.

Goods and Services Tax (GST)

A reconciliation of GST should be performed as at 30 June 2017 to determine if there has been an under or over-payment of GST in the 2017 tax year. If a discrepancy has arisen, then it is possible to adjust a subsequent Business Activity Statement (BAS) to rectify the error, however there are limits imposed on adjustments that can be made in this way.

Income declared on your BAS should be reconciled to income declared on your income tax returns.

Also, please note that you are required by law to substantiate all Input Tax Credit claims with a complying Tax Invoice, and you need to retain these documents for a minimum of 5 years.

(Action Required) Complete the annual GST reconciliations, and check that you have all required tax invoices and other supporting documents.

ATO Audit Activity

Please note that the ATO and State Revenue Office are constantly increasing their audit activities. There has been an increase in audit activity for PAYG Withholding, Payroll Tax, WorkCover, GST, Division 7A loan accounts from companies, and Trust distributions from Discretionary Trusts.

We can offer a review of your records and record-keeping procedures if you are concerned about your ability to satisfy an audit.

(Action Required) Please contact our office if you would like to request this service.

Last Minute Tax Minimisation Tips

Here’s a few final reminders about ways to reduce your tax for 2017:

1. Write-off Bad Debts

2. Write-off any trading stock that is damaged or obsolete

3. Review your Asset Register and scrap any obsolete plant and equipment

4. Pay for marketing materials, repairs, consumables, office stationery, and donations before 30 June 2017

5. Ensure employee superannuation contributions are made (and received by your employees’ superannuation fund/s) by 30 June 2017 to allow a tax deduction this financial year

6. Realise any capital losses you have before 30 June 2017 to offset against any capital gains you may have made

7. Review the guidance provided in TR97/7 to confirm if you are eligible to claim deductions for your creditors as at 30 June 2017

General Advice Disclaimer

General advice warning: The advice provided is general advice only as, in preparing it we did not take into account your investment objectives, financial situation or particular needs. Before making an investment decision on the basis of this advice, you should consider how appropriate the advice is to your particular investment needs, and objectives. You should also consider the relevant Product Disclosure Statement before making any decision relating to a financial product.

Did you like this article? Email it to a friend

{kind=link}